The NVDA Hallucination: Recovering the Missing 0.877

Audit Log #005

The NVDA Hallucination:

Recovering the Missing 0.877

"YOUR CLIENT SEES +763%. YOU SEE A POTENTIAL 1099-B HALLUCINATION."

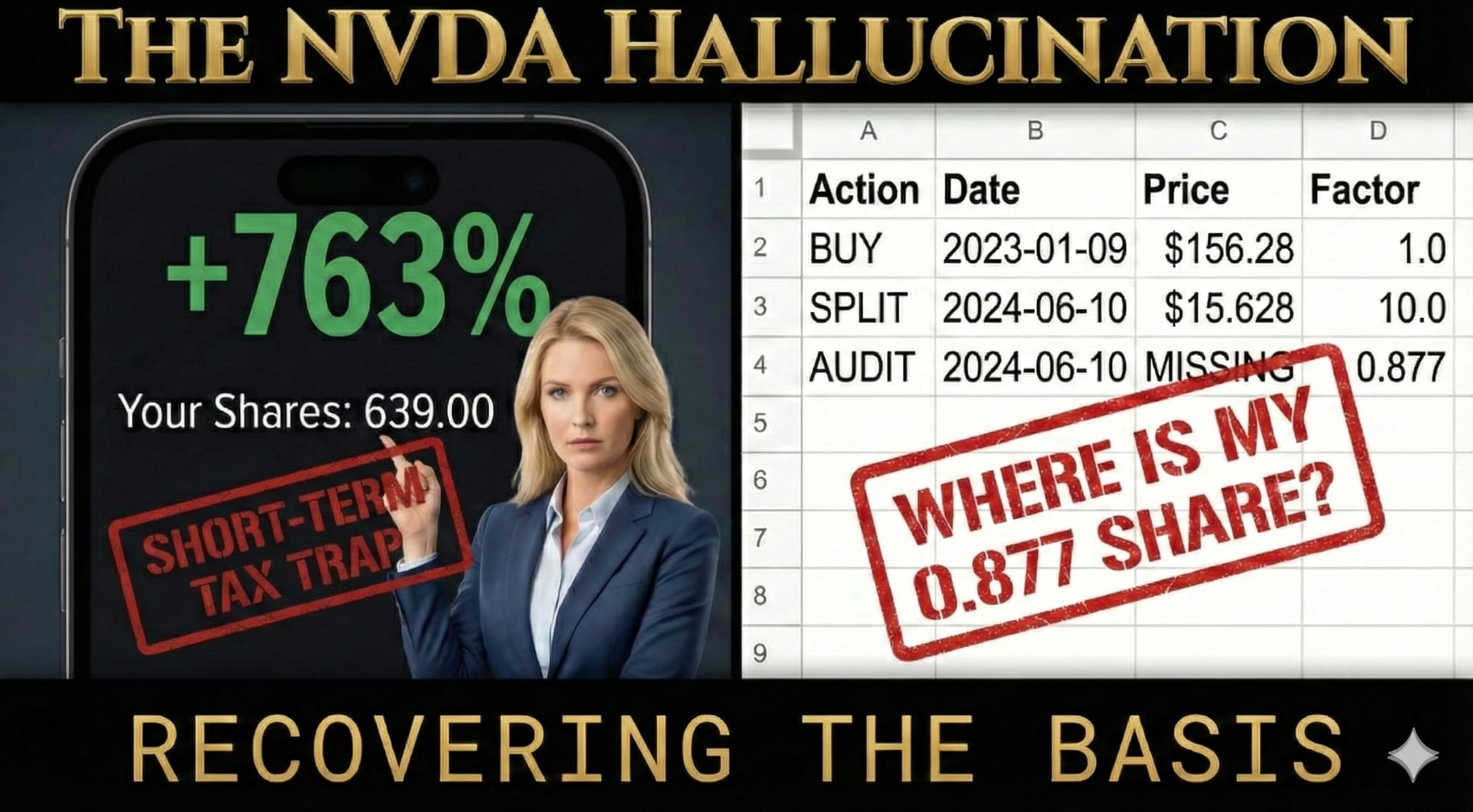

*Exhibit A: The $NVDA 10:1 Split and the systemic disappearance of fractional cost basis.

The 0.877 Fragment Heist

When NVIDIA executed its 10:1 split, millions of retail accounts were flooded with "Green Euphoria." But beneath the +763% gains shown in brokerage apps, a silent professional liability was taking root.

Look at the data. The broker reported 639.00 shares. But the original DNA demanded 639.877. That 0.877 fragment was forcibly liquidated as "Cash in Lieu" (CIL). In the chaos, most 1099-Bs reported the cost basis for this fragment as $0.00.

To a broker, it’s a rounding error. To an IRS auditor, it’s an unexplained gain. To a sophisticated practitioner, it’s a failure of fiduciary duty.

WATCH: SURGICAL RECOVERY

See FDL reconstruct the 2022 DNA and restore the missing $13.71 basis.

Forensic Audit: Target Lot [NVDA-20221020-01]

- FRACTIONAL BASIS (0.877): $0.00 (Abandoned)

- HOLDING PERIOD: Short-Term (Reset)

- GAIN %: +763% (Passive Hook)

- RECOVERED BASIS (0.877): $13.71 (Restored)

- HOLDING PERIOD: Long-Term (DNA Preserved)

- TAX STATUS: Audit-Defensible Fact

🏛️ UNDER THE HOOD: Tax-Logic Granularity

FDL does not merely "resize" quantities; it deciphers the substantive tax DNA of each event. The allocation of Cash-in-Lieu (CIL) is not a universal constant.

FDL’s engine enforces the surgical distinction between a Stock Split (IRC §305) and a Tax-Free Reorganization (IRC §354, 356).

Restore the Reality

Don't let a brokerage algorithm dictate your client’s tax liability. Reclaim your agency from passive defaults. FinDash Lens: The Registry of Truth for practitioners who demand absolute control.