GE Spin-Off Cost Basis and Holding Period | GE, GEHC, GEV

PROOF LOG #010

GE Spin-Off Cost Basis and Holding Period | GE, GEHC, GEV

A reverse split and dual spin-off did not erase history. The broker-facing record did not preserve the full lot history.

GE was not a ticker change.

It was a structural event chain.

FDL does not guess the aftermath.

It restores the original record.

EXECUTIVE PROOF

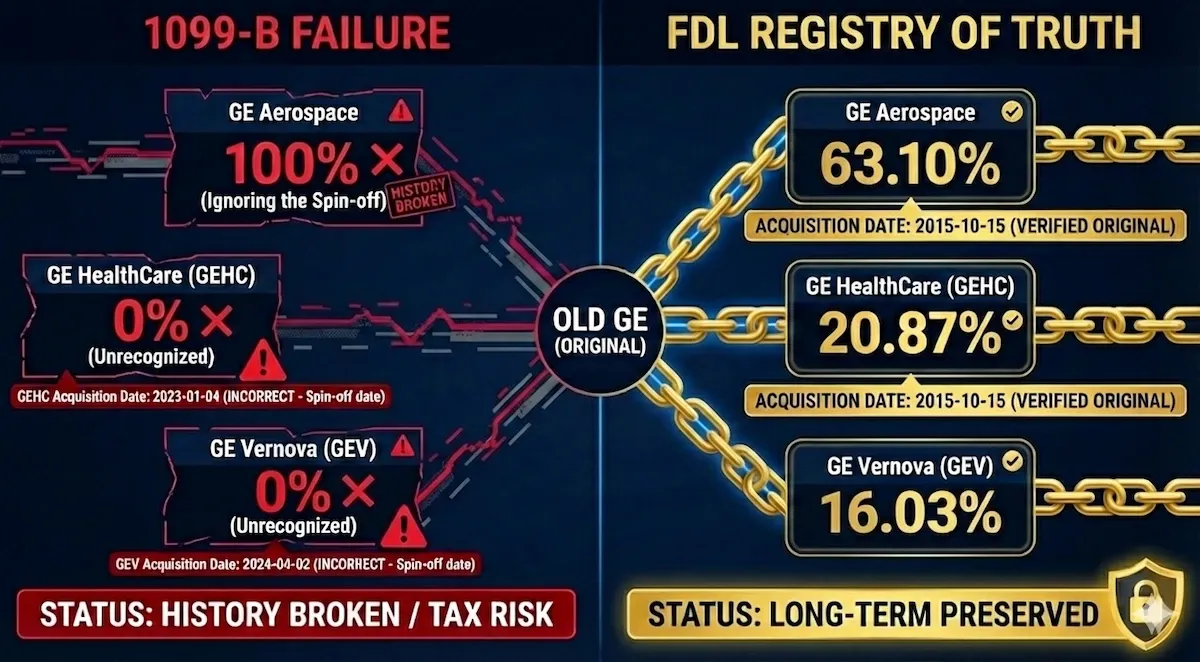

1099-B / Broker View

- basis links collapse

- lineage breaks across the split and spin-offs

- holding period continuity becomes unreliable

- the operator is left reconciling fragments

FDL Registry of Truth™

- original GE ancestry is preserved

- basis is re-anchored across GE / GEHC / GEV

- holding period continuity remains visible

- every result is traceable to a deterministic audit path

WATCH THE RECONSTRUCTION

Watch the chain being rebuilt.

- reverse split accounted for

- GE / GEHC / GEV basis chain restored

- historical lineage preserved across the event sequence

- the result becomes reviewable, not guessed

PHASE 1 — THE BREAK

The event did not break the history.

The record did.

Across the reverse split and spin-off sequence, broker-facing records can fragment the visible ancestry, basis, and holding-period continuity.

What looks complete can still be structurally wrong.

PHASE 2 — THE RE-ANCHORING

FDL does not start from the fragments.

It starts from the original lot.

The chain is rebuilt forward, so ancestry, basis, and continuity remain reviewable across GE / GEHC / GEV.

FDL does not manufacture a new story.

It restores the old one.

FORENSIC EVIDENCE

What must remain intact

- Acquisition continuityThe date chain must remain anchored to pre-event history.

- Basis continuityCost basis must remain connected across the successor positions.

- Holding-period continuityThe event must not silently sever the maturity of the original lot.

What FDL makes legible

- Tax ReportShows the tax result.

- Audit TrailRecords lot lineage, basis movement, and IRC-aligned citations.

- Tax Alpha DashboardShows where preserved or recoverable value sits.

This is the point of the white-box architecture:

not just to compute, but to separate result, trace, and value visibility.

WHY THIS CASE MATTERS

This is not a cosmetic discrepancy.

It is a broken chain beneath an apparently complete file.

That is where audit risk begins.

This is where FDL is strongest.

WHAT FDL IS SHOWING HERE

FDL is not guessing the outcome.

It is restoring the record that the event requires.

Result, trace, and value visibility are separated so the file can be reviewed, not merely accepted.

CHOOSE YOUR NEXT STEP

FDL — deterministic tax infrastructure for prepared, in-scope records.